If you live in or have visited a big city, you’ve probably run into street vendors – people who sell everything from hot dogs to umbrellas in carts on the streets and sidewalks. Many of these entrepreneurs sell completely unrelated products, such as coffee and ice cream. At first glance, this approach seems a bit odd, but it turns out to be quite clever. When the weather is cold, it’s easier to sell hot cups of coffee. When the weather is hot, it’s easier to sell ice cream. By selling both, vendors reduce the risk of losing money on any given day.

Asset Allocation

Asset allocation applies this same concept to managing investment risk. Under this approach, investors divide their money among different asset classes, such as stocks, bonds, and cash alternatives, like money market accounts. These asset classes have different risk profiles and potential returns.¹

The idea behind asset allocation is to offset any losses in one class with gains in another, and thus reduce the overall risk of the portfolio. It’s important to remember that asset allocation is an approach to help manage investment risk. It does not guarantee against investment loss.²

Determining the Most Appropriate Mix

The most appropriate asset allocation will depend on an individual’s situation. Among other considerations, it may be determined by two broad factors:

- Time. Investors with longer time frames may be comfortable with investments that offer higher potential returns but also carry higher risk. A longer time frame may allow individuals to ride out the market’s ups and downs. An investor with a shorter time frame may need to consider market volatility when evaluating various investment choices.

- Risk tolerance. An investor with high risk tolerance may be more willing to accept greater market volatility in the pursuit of potential returns. An investor with a low risk tolerance may be willing to forego some potential return in favor of investments that attempt to limit price swings.

Asset allocation is a critical building block when creating a portfolio. Having a strong knowledge of the concept may help as you consider which investments may be appropriate for your long-term strategy.

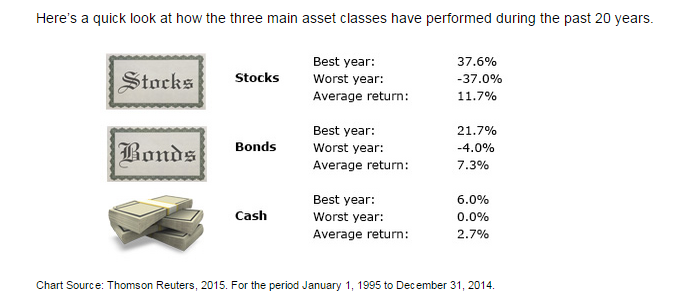

Stocks are represented by the S&P 500 Composite Index (total return), an unmanaged index that is generally considered representative of the U.S. stock market. The return and principal value of stock prices will fluctuate as market conditions change. And shares, when sold, may be worth much more or less than their original cost.

Bonds are represented by the Citigroup Corporate Bond Composite Index, an unmanaged index that is generally considered representative of the U.S. bond market. The market value of a bond will fluctuate with changes in interest rates. As rates rise, the value of existing bonds typically falls. If an investor sells a bond before maturity, it may be worth more or less than the initial purchase price. By holding a bond to maturity, investors will receive the interest payments due plus their original principal, barring default by the issuer.

Cash is represented by the Citigroup 3-Month Treasury-Bill Index, an unmanaged index that is generally considered representative of short-term cash alternatives. U.S. Treasury bills are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury bill prior to maturity, it could be worth more or less than the original price paid.

Investments seeking to achieve higher potential returns also involve a high degree of risk. Past performance does not guarantee future results. Actual results may vary.

¹ The return and principal value of stock prices will fluctuate as market conditions change. And shares, when sold, may be worth more or less than their original cost. The market value of a bond will fluctuate with changes in interest rates. As rates rise, the value of existing bonds typically fails. The market value of a bond will fluctuate with changes in interest rates. As rates rise, the value of existing typically falls. If an investor sells a bond before maturity, it may be worth more or less that the initial purchase price. By holding a bond to maturity investors will receive the interest payments due plus their original principal, barring default by the issuer. Money market funds seek to preserve the value of your investment at $1.00 a share. Money held in money market funds is not insured or guaranteed by the FDIC or any other government agency. It’s possible to lose money by investing in a money market fund. Mutual funds are sold by prospectus. Please consider the charged, risks, expenses, and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

² Investments seeking to achieve higher potential returns also involve a high degree of risk. Past performance does not guarantee future results. Actual results will vary.

Copyright 2015 FMG Suite.

Back